EUR/USD

1.14088

0.098%

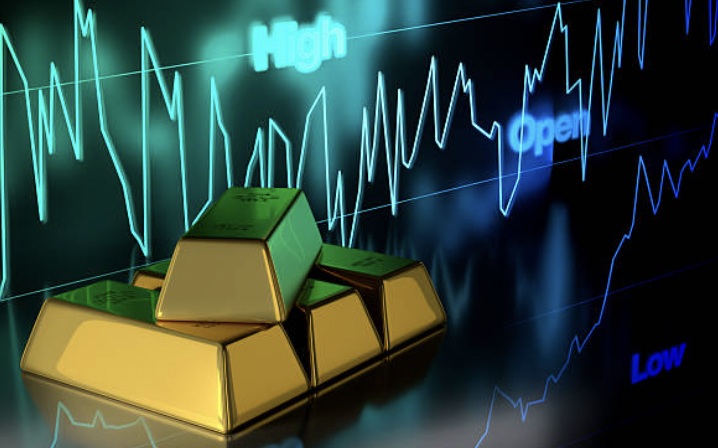

Gold

4147.17

1.706%

Oil

85.662

1.740%

USD/JPY

163.091

-0.058%

GBP/USD

1.33710

-0.024%

GBP/JPY

218.074

-0.069%

On July 23, Wang Yi stated that Prime Minister Tariqs successful official visit to China last month, during which the leaders of both countries jointly announced the building of a China-Bangladesh community with a shared future in the new era, provided new strategic guidance and outlined a new blueprint for the development of bilateral relations. As a trustworthy neighbor and good friend of Bangladesh, China will, as always, support the Bangladeshi government in its smooth governance and is willing to work with Bangladesh to implement the consensus reached by the leaders of the two countries, enhance strategic communication, deepen political mutual trust, promote high-quality Belt and Road cooperation, and push forward the building of a China-Bangladesh community with a shared future in the new era, bringing more benefits to the people of both countries. Khalid stated that Bangladesh firmly adheres to the one-China principle and is willing to work with China to implement the outcomes of this visit, advance cooperation such as the China-Myanmar-Bangladesh Economic Corridor, and jointly build a China-Bangladesh community with a shared future in the new era.The Israel Defense Forces (IDF) stopped and detained several Israeli citizens attempting to cross the border into Syria in the Hermon region on Wednesday, local time. The IDF condemned this "criminal" act that endangered border security.July 23 – First, the building of a community with a shared future with neighboring countries has deepened and become more practical. China and the eight ASEAN countries have reached an important consensus on jointly building a bilateral community with a shared future, further solidifying the foundation for building a closer China-ASEAN community with a shared future. Second, trade volume has steadily increased. The upgraded protocol of the China-ASEAN Free Trade Area 3.0 was officially signed, and the two sides have been each others largest trading partners for six consecutive years, with trade volume expected to exceed one trillion US dollars by 2025. Third, cooperation has been strengthened to overcome difficulties. After the strong earthquake in Myanmar and the earthquake in Mindanao, Philippines, China provided immediate assistance, demonstrating the fine tradition of mutual support between China and ASEAN countries. Fourth, people-to-people exchanges have become more active. The China-ASEAN Year of People-to-People Exchanges (2024-2025) will host nearly 200 high-level and popular events. China has introduced a special "ASEAN Visa" to facilitate and enhance people-to-people exchanges, further strengthening the people-to-people ties between the two sides.British Chancellor of the Exchequer Healy: The goal is to improve affordability.British Chancellor of the Exchequer Healy: I will support wealth creation.